Forecasting Volatility With GARCH Model-Volatility Analysis in Python

Harbourfront Technologies

185

1:59

Oct 26, 2020

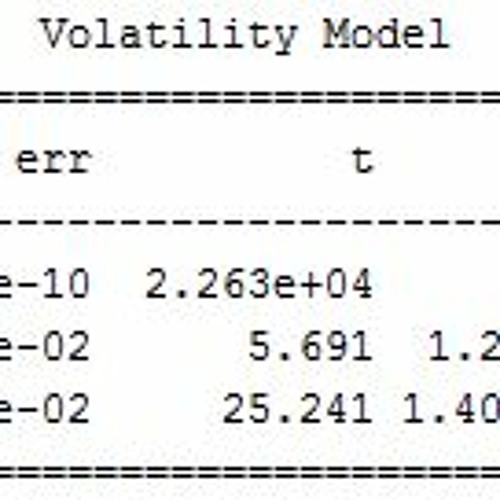

In a previous post, we presented an example of volatility analysis using Close-to-Close historical volatility. In this post, we are going to use the Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model…